America is facing a retirement crisis. Surveys conducted by the Federal Reserve have found that only 75% of non-retirees have any retirement savings whatsoever, and only 40% feel that their retirement savings are on track.

Secure Act 2.0 is Congress’s latest attempt to address this pressing issue. Signed into law in late December 2022, this package of retirement reforms aim to finish the job begun by the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019.

Version 2.0 of the Secure Act introduces dozens of provisions intended to improve retirement outcomes. From better catch-up contributions to automatic 401(k) enrollment.

Join Relation Insurance and ERISSA expert Brad Campbell as they help you understand the important implications for both employers and employees.

About The Speakers

April Is Distracted Driving Awareness Month. The National Safety Council recognizes April as Distracted Driving Awareness Month to help raise awareness about the dangers of distracted driving and encourage motorists like you to minimize potential distractions behind the wheel. Learn more on ways you can help prevent distracted driving.

Distracted Driving Overview

According to the Centers for Disease Control and Prevention, distracted driving refers to any activity that may divert a motorist’s attention from the road. There are three main types of distractions that can interfere with drivers’ attentiveness behind the wheel, including:

Visual distractions

These distractions involve motorists taking their eyes off the road. Some examples of visual distractions include reading emails or text messages, focusing on vehicle passengers, looking at maps or navigation systems, and observing nearby activities (e.g., accidents, traffic stops or roadside attractions) while driving.

Manual distractions

Such distractions entail motorists removing their hands from the steering wheel. Key examples of manual distractions include texting, adjusting the radio, programming navigation systems, eating, drinking or performing personal grooming tasks (e.g., applying makeup) while driving.

Cognitive distractions

These distractions stem from motorists taking their minds off driving. Primary examples of cognitive distractions include talking on the phone, conversing with vehicle passengers or daydreaming while driving.

Regardless of distraction type, distracted driving is a serious safety hazard that contributes to a significant number of accidents on the road. In fact, the National Highway Traffic Safety Administration reported that more than 2,800 people are killed and 400,000 are injured in crashes involving a distracted driver each year—equating to approximately eight deaths and 1,095 injuries per day. Considering these findings, it’s crucial to take steps to prevent distracted driving.

Distracted Driving Prevention Tips

Whenever you get behind the wheel, keep these distracted driving prevention measures in mind:

- Put away your phone. Silence your phone and store it in a location that is out of reach while driving to lower the temptation to check it.

- Plan your trip before you leave. Program your navigation system prior to hitting the road to get familiar with your journey and feel confident in your route.

- Don’t fumble with your playlist. Select a radio station or plug in a predetermined playlist before driving to limit the need for music adjustments.

- Secure passengers. Ensure kids are properly situated in car seats (if needed) with seat belts fastened. Keep pets stationary in the back seat.

- Avoid multitasking. Never complete additional tasks—such as eating or personal grooming—behind the wheel.

- Stay focused. Concentrate your mind on the road by keeping distracting conversations to a minimum and looking straight ahead.

This article is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel or an insurance professional at Relation Insurance for appropriate advice.

©2023 Zywave,Inc. All rights reserved.

Recent market developments have demonstrated signs of an improving commercial insurance landscape. Yet, industry experts asserted that ongoing headwinds facing certain lines of coverage will continue to generate hardened conditions overall, therefore driving up premiums. As such, it’s essential for businesses to be aware of the following market trends and how they may impact coverage costs:

Labor shortages trends impacting commercial insurance costs

The last few years have seen widespread labor shortages, largely stemming from employees adjusting their job priorities in response to the COVID-19 pandemic. Such shortages have motivated some businesses to hire less experienced workers and place extra demands on existing employees to fill labor gaps; however, doing so can heighten liability exposures and increase the risk of workplace accidents, paving the way for rate jumps in several commercial insurance segments.

Supply chain disruptions trends impacting commercial insurance costs

Continued pandemic-related challenges, global transportation breakdowns and commercial driver shortages have slowed shipment and delivery times for many high-demand goods, creating supply chain issues for businesses across industry lines. These issues have led to considerable disruptions, prolonged recovery times, compounded claim expenses and elevated premiums in multiple commercial insurance segments.

Inflation issues trends impacting commercial insurance costs

In recent years, labor shortages and supply chain issues have fueled rising inflation concerns throughout the commercial insurance space, as evidenced by a surging consumer price index (CPI). Altogether, the elevated CPI has driven up claim costs, inflated total loss expenses and prompted rate hikes for various lines of coverage.

Recession risks trends impacting commercial insurance costs

Some economic experts have forecasted that the United States is headed toward a recession in the near future. During a recession, businesses usually experience decreased sales and profits, which may cause them to reduce their workforces and cut their spending to help maintain financial stability. Although having fewer employees could minimize occupational injuries and associated claims, limited funding for risk management and cybersecurity initiatives may create further liability exposures, making busi- nesses more vulnerable to increased losses and higher commercial insurance premiums.

Social inflation trends impacting commercial insurance costs

Social inflation refers to societal trends that push insurance costs above the overall inflation rate. Current drivers of social inflation include increased third-party litigation funding and the rise of anti-corporate culture. Amid these trends, businesses have been held more ac- countable for their wrongdoings, sometimes resulting in nuclear verdicts (jury awards exceeding $10 million). Social inflation has been a main factor in rising claim severity and rate jumps across many commercial insurance segments.

Extreme weather events impacting commercial insurance costs

Natural disasters (e.g., hurricanes, tornadoes, hailstorms and wildfires) continue to make headlines as they become increasingly devastating and costly. Making matters worse, these events aren’t limited to one geographic area; they impact establishments across the United States. Natural disasters have left businesses with significant repair and re- placement expenses, exacerbating losses and resulting in higher commercial insurance premiums.

During these challenging times, we are here to provide much-needed market expertise. Contact us today for additional risk management guidance and insurance solutions.

This article is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel or an insurance professional at Relation Insurance for appropriate advice.

©2023 Zywave,Inc. All rights reserved.

The current state of the world has made it more important than ever for employers to align with employees in all aspects of their lives.

Join Relation Insurance and Franklin Templeton as they help you:

- Identify why there has never been a more urgent time for employers to evaluate their benefit offerings and consider ways to evolve the way they support employee needs

- Understand how personalization has empowered consumers and is becoming the market standard

- Understand the lack of employee well-being has an impact on their work

- Recognize that workers are looking to their employers for help

Speakers:

President Biden Discusses Employee Benefits and the Workplace in State of the Union Address

On Tuesday, Feb. 7, President Joe Biden delivered the 2023 State of the Union (SOTU) address. The SOTU address is an annual speech the president delivers near the beginning of each year, outlining how the country is doing and identifying future initiatives the current administration wants to pursue. For employers, the SOTU address is important as it often provides insight into proposed plans and initiatives relevant to the workplace. The 2023 SOTU address focused on health care and the economy. Read on for the main takeaways from the speech.

“Let’s also make sure working parents can afford to raise a family with sick days, paid family and medical leave, and affordable child care that will enable millions more people to go to work.”

– President Biden, in the SOTU address

Workplace Changes

President Biden pushed for passing the Protecting the Right to Organize Act (or PRO Act), which strengthens the federal laws protecting employees’ rights to organize and collectively bargain.

Additionally, the administration advocated for sick days, paid family and medical leave and affordable child care. He also mentioned a need to restore the full child tax credit to offer parents more breathing room. President Biden stressed that steps must be taken to help working parents afford to raise a family and access more benefits. Ultimately, it was a call for guaranteeing all workers a living wage.

The administration is also moving to ban noncompete agreements to make organizations compete for workers and pay them what they’re worth, removing time limitations on industries or companies after leaving a job.

Health Care Prices

While progress has been made in lowering health care costs, there is still more work to be done. President Biden outlined steps to strengthen Medicare, Medicaid and the Affordable Care Act (or ACA), as well as give more families the peace of mind of affordable health care.

If drug companies hike prescription drug prices faster than inflation, they will have to pay the difference back to Medicare. And as part of a new prescription drug law that goes into effect in 2025, Medicare will cap out-of-pocket pharmacy costs at $2,000 per year under Part D. Such changes are intended to help elderly individuals save more on their health care-related expenses. Additionally, Medicare beneficiaries will pay no more than$35 per month per insulin prescription. President Biden called on Congress to extend this protection to all Americans.

Mental Health Crisis

One of the more detailed talking points in last year’s SOTU address focused on handling the mental health crisis and the White House’s related implementation strategy. While the administration made strides in 2022, including launching the 988 National Suicide and Crisis Lifeline and helping address the negative impacts of social media on today’s youth, it plans to continue tackling the mental health crisis in 2023 by:

- Creating healthy environments, such as safe online platforms for children and resources to support and build resilience in the health care workforce

- Connecting more Americans to care (e.g., affordable and accessible health insurance, integrated mental health services in schools and expanded telehealth access)

- Strengthening health care system capacity as the nation experiences a behavioral health professional shortage

Mental health is a serious concern for many Americans. The COVID-19 pandemic significantly impacted individuals’ mental health and substance use, with such challenges likely to continue as the country navigates economic uncertainty.

Veteran Support

Over the past year, the administration has expanded benefits for veterans, their caregivers and survivors. In 2022, the Department of Veterans Affairs processed a record 1.7 million veteran claims and delivered $128 billion in earned benefits to 6.1 million veterans and survivors. The administration plans to continue those efforts by focusing on:

- Reducing veteran suicide

- Expanding access to peer support, including mental health services

- Ensuring access to affordable, stable housing for low-income veterans

- Delivering job training for veterans and their spouses

Overall, these plans are meant to expand support and outreach to help the nation’s veterans.

Reproductive Health and Equality

President Biden called on Congress to protect people’s rights and freedoms. First, he urged Congress to restore the right the Supreme Court took away last year and codify Roe v. Wade. As more than a dozen states enforce abortion bans, President Biden reinforced that he would veto any national abortion ban passed by Congress.

Additionally, the administration called for Congress to pass the Equality Act to ensure LGBTQ Americans, especially young transgender people, can live safely.

Opioid and Overdose Epidemic

Another significant health care talking point involved the opioid and overdose epidemic. While overdose deaths and poisonings have decreased for five consecutive months, these drug-related deaths remain high and are primarily caused by fentanyl. As a result, the administration plans to address this by:

- Disrupting the trafficking, distribution and sale of fentanyl

- Expanding access to prevention, treatment and recovery for substance use disorders

President Biden also highlighted the Mainstreaming Addiction Treatment Act (or MAT Act) passing, which removes barriers for health care providers prescribing life-saving medications for opioid use.

Cancer Moonshot

Cancer remains the second leading cause of death in America. Last year, President Biden announced a plan to “supercharge the Cancer Moonshot,” a program that aims to cut cancer’s death rate by at least half over the next 25 years and improve the experience of people and their families living with and surviving cancer. Over the past year, Cancer Moonshot announced nearly 30 new federal programs, policies and resources to close gaps, decrease preventable cancers and support patients and caregivers.

President Biden called on Congress to drive further progress this year by:

- Urging the reauthorization of the National Cancer Act to update and modernize the nation’s cancer research and care systems

- Ensuring patient navigation services are covered benefits going forward for as many people as possible

- Helping people avoid smoking in the first place and supporting Americans who want to quit

Additionally, President Biden and Congress have already provided an initial investment of $2.5 billion to fund the Advanced Research Projects Agency for Health (ARPA-H) to drive breakthroughs in cancer, Alzheimer’s disease, diabetes and other diseases. The Inflation Reduction Act will also lower prescription drug costs for thousands of cancer patients with Medicare coverage.

Economic Recovery

Part of the administration’s efforts for a strong economic recovery includes bringing manufacturing operations back to the United States. Additionally, President Biden touted the Junk Fee Prevention Act to stop excessive junk fees, which are hidden surcharges from companies associated with the purchase of their products or services. Junk fees can make it more challenging for Americans to pay their bills or afford other expenses.

COVID-19 Emergency Periods

Prior to the SOTU address, the administration announced plans to end the COVID-19 public health emergency (PHE) and national emergency on May 11, 2023. The end of the COVID-19 emergency periods triggers the end of numerous measures related to the federal government’s pandemic response, including some requirements for employer-sponsored health plans. For example, when the PHE ends, health plans will no longer be required to cover COVID-19 diagnostic tests and related services without cost sharing. Non-grandfathered health plans will still be required to cover recommended preventive services, including COVID-19 immunizations, without cost sharing; however, this coverage requirement will be limited to in-network providers.

What’s Next?

The SOTU address serves mainly as a presidential wish list; it’s a chance for the current administration to outline where it wants to take the country over the next year. It’s unreasonable to speculate on how some of the agenda items may take shape at this time. As such, employers should look for more details about the SOTU proposals in the coming weeks and months. While some of the discussed initiatives have the potential to significantly affect the workplace, these impacts won’t be evident until more information is released.

Relation Insurance Services will keep you apprised of any additional government updates and other pertinent matters. In the meantime, contact us for additional workplace guidance.

The content of this News Brief is of general interest and is not intended to apply to specific circumstances. It should not be regarded as legal advice and not be relied upon as such. In relation to any particular problem which they may have, readers are advised to seek specific advice. © 2023 Zywave, Inc. All rights reserved.

Join our Employee Benefits team for our latest compliance webinar:

Wellness Programs And The Law: Checking The Boxes

Setting up a wellness program requires many steps beyond developing options and strategies that will increase the health and well-being of your employees. A major hurdle is satisfying all of the legal requirements that apply. This program will provide an overview of the main legal requirements impacting wellness programs (HIPAA, ADA, and GINA), and provide guidance on developing a compliant program. We will discuss common compliance challenges facing employers and offer some solutions. Tips, traps, best practices, and action items will be included.

Date: Wednesday, February 22, 2023

Time: 2 PM EST

Duration: 1 hour 30 minutes

Have questions? Please feel free to submit them in advance to [email protected] or questions may be asked during the webinar.

After you register, you will receive a confidential email containing information about joining the meeting. Be sure to add the event to your calendar.

With the new SECURE Act 2.0 up for review in the Senate, now is the time for HR professionals to get proactive about setting employees up for a successful retirement in the new landscape of retirement planning.

Our team of Retirement specialists broke down the most notable features of the SECURE Act 2.0 to help you and your team prepare.

The original SECURE Act (Setting Every Community Up for Retirement Enhancement) was passed in 2019 and went into effect in 2020. Its intent was to help employers offer retirement plans that empower workers at all income levels to save for their futures. Now, two years later, further reforms may be signed into law in a matter of months or even weeks.

Here’s what you need to know about the SECURE Act 2.0 and how it will affect your employees:

Raising the age of the Required Minimum Distribution (RMD.)

The age at which an individual is required to start drawing money out of their pre-taxed retirement accounts is going up. The first SECURE Act raised the age from 71.5 to age 72, and the new version includes a plan that extends it to age 73 in 2023, then to age 74 in 2030, and finally to age 75 in 2033. This is overall a positive change because individuals are no longer forced to take money out as early. Of course, if they want to, then they can, but it is not required.

The penalty for missing the RMD is less severe.

While it is still significant, the SECURE Act 2.0 lowers the penalty for missing the RMD. In the scenario that an individual forgets to take money out from their retirement account, the penalty will be decreased. For example: In the past, if an individual was required to take out $10,000 from an IRA and forgot to do so, the penalty was 50%. So, that person would still have to take the $10,000 out, report it on their taxes, and then pay a $5000 penalty. The new SECURE Act 2.0 drops the penalty to 25%.

Auto-enrollments.

The SECURE Act 2.0 requires auto-enrollment to new employees. When a new hire starts at your company, they will automatically be enrolled in the firm’s retirement program at 3%. There is also an auto-increase feature, increasing the contribution each year by 1% until it reaches 10%. Of course, employees may opt to put in any amount they’d like, but this move ensures that the default for all employees is to contribute. While this is a great feature for many employees who would otherwise forget to enroll, this amount is often not enough for an individual to set up a successful retirement plan. There’s a chance this handy set-it-and-forget-it policy could leave some employees wondering why their nest egg isn’t what it needs to be.

Increased catch-up contributions.

Under the current law, an individual is allowed to contribute more toward their retirement once they turn 50. With the SECURE Act 2.0, this allowance is increased at ages 62, 63, and 64. All catch-up contributions will be considered Roth contributions, which means the individual will pay taxes on them upfront. This new rule is helpful in that it gives individuals the ability to save more in that final push to prepare for retirement.

Retirement Savers’ Contribution Credit.

We love this one. This credit is a dollar-for-dollar reduction that an individual does not need to pay back. It really is a tax credit just for saving up for retirement, which employees should be doing anyway. For those who are eligible, the credit is 50% per person – which means, if they are married, their spouse could likely take the same credit. That’s a win!

Student loans.

This adjustment to the SECURE Act is about – you guessed it – matching contributions to student loan payments. As an employer, you may already have a program where you already pay or match your employees’ student loan payments. It appears that this new feature would make it so that these matches can go straight into the employees’ 401(k). This could be a great asset to recruitment for those employees who are not able to make both a student loan payment and a 401(k) contribution.

More potential Roth contributions.

Currently, the employer match on retirement contributions goes into the traditional 401(k). However, in the SECURE Act 2.0, employer-matching contributions will be allowed to be made as Roth contributions. This is helpful for employees in low tax brackets saving up for Roth, as another way to get more dollars in their Roth 401(k), growing tax-free for their financial future.

Employers are now allowed to incentivize employees to participate in their retirement plan.

Finally, employers are now able to encourage employees to participate in their retirement program by providing incentives, such as small gift cards. Any token that reminds an employee to participate is a win for both the employee and the employer.

In summary, the SECURE Act 2.0 provides more options for retirees, but the new rules can be a little complex. We recommend preparing communications for employees ahead of time so they can start thinking about their new landscape of retirement planning.

This is a great time for HR Professionals to review their company retirement programs and make changes to successfully recruit and retire valued employees. For an assessment of your current plan, guidance on choosing a new plan, or questions regarding the SECURE Act 2.0 or other retirement-related questions, please reach out to our Retirement team.

[hubspot type=”form” portal=”7375193″ id=”fc505768-dc0c-4d81-942d-d86c55a59363″]

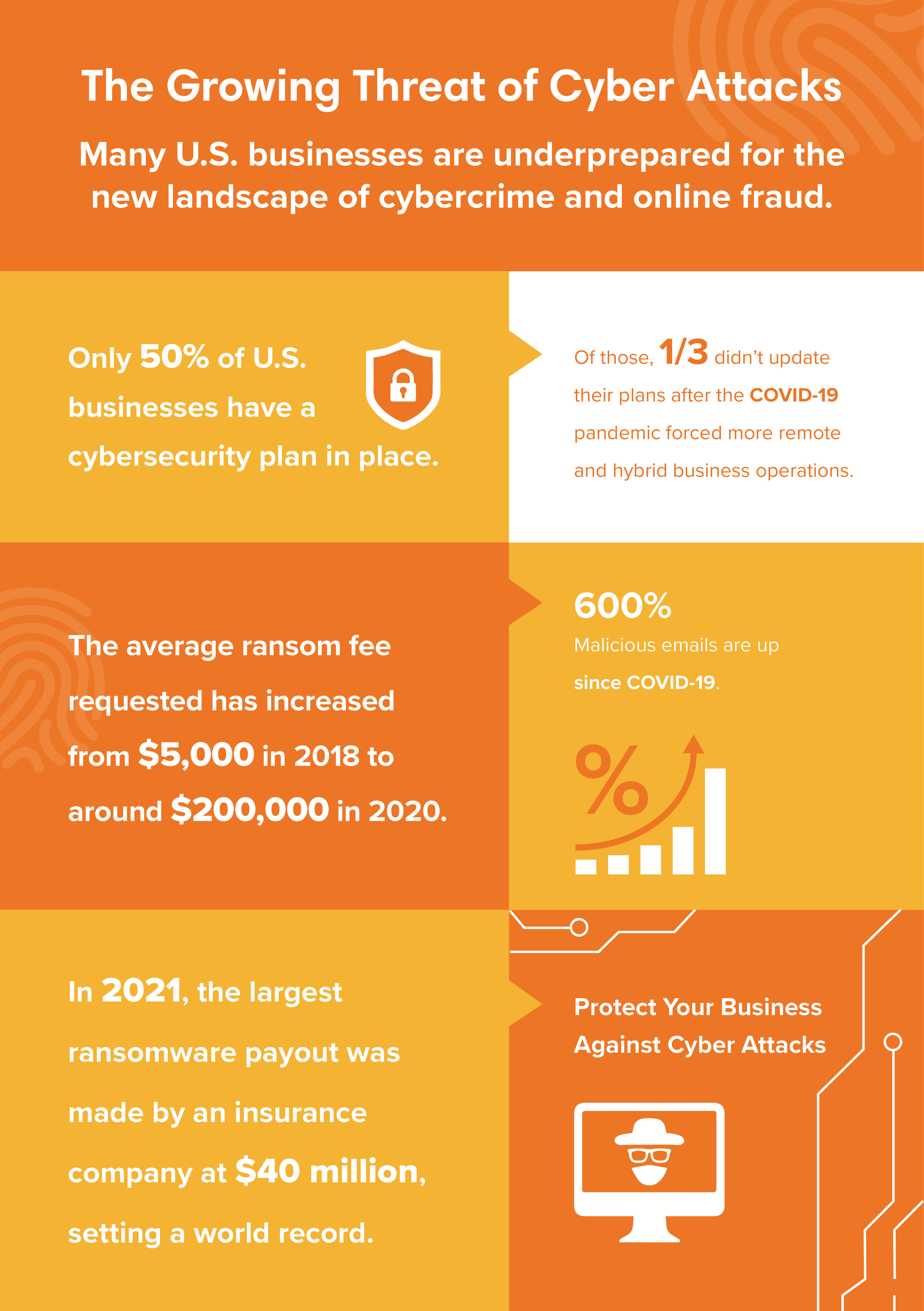

October is National Cybersecurity Awareness Month, and as the world grows digitally, cybercrime and online fraud are becoming more complex. Our experts have put together a helpful guide for you to assess your cyber risk and whether you may need to update your cybersecurity plan in order to protect your business against cyber attacks.

Do you have a cybersecurity plan in place?

Only half of all businesses in the United States have a cybersecurity plan in place – a shockingly low proportion, considering that cyber attacks do not discriminate. Every business, large and small, is a target. If you do not have a plan in place, now is the time to create one. (If you’re not sure where to start, you can reach out to a cybersecurity specialist for a free consultation!)

When was the last time you updated your cybersecurity plan?

Of the businesses that have a plan for cybersecurity, a third have never updated their plans after the increase in remote and hybrid work operations that came with COVID-19 in 2020. At a time when exposure and risk is rising exponentially, it’s imperative to revamp your cybersecurity plan. Experts recommend reviewing and adjusting your plan at least once per year to protect your business against the latest malware and cyber attack strategies.

How do you keep your team aware of online threats that could put your business at risk?

Malicious emails have increased a whopping 600% since 2020. At the same time, ransomware is becoming more aggressive, with the average requested fee going from $5K in 2018 to $200K in 2020. It only takes one slip-up by a well-meaning team member to take down everything you’ve worked so hard to build. Make sure your whole team is educated on what cyber threats can look like and what to do if faced with a potential risk.

How does your website expose you to risk?

As cybercrime evolves, it’s important to know how your website holds up against current threats. Through our cybersecurity team and partners, we can put your site to the test against potential threats, so you can know where you stand, and we can work together to mitigate your risk.

What cyber protection is common practice for your industry and company size?

Discover how your competitors and others in your industry are protecting themselves. Using our cyber protection partner’s benchmarking tool, we can review the typical coverage of your industry for a company your size, so you’ll know exactly how you stack up.

What is your existing cyber liability, and which coverage is right for your business?

That’s what we’re here to help you find out. When you work with us to manage your cyber risk, our cybersecurity experts and partners analyze and assess the entirety of your cyber risk and build a custom program from the ground up. Our goal is to protect what you’ve built.

Cyber risks aren’t going away. But we’re here to help. We believe every business should be protected and our team is ready to partner with you to ensure your business has what it takes to stay safe online.

Contact our Cyber Security experts for a free consultation and protect your business against cyber attacks.

[hubspot type=”form” portal=”7375193″ id=”fc505768-dc0c-4d81-942d-d86c55a59363″]